Lion Finance is heading to the big league, and this once-peripheral story is one worth knowing

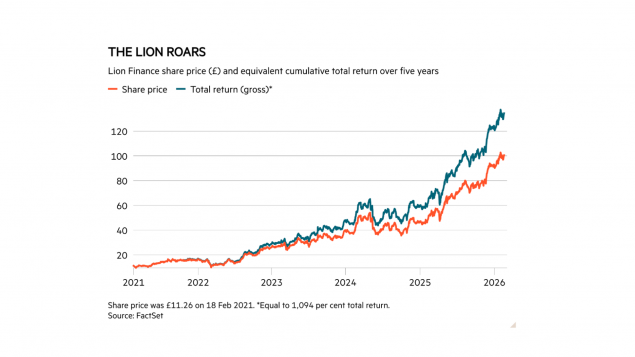

Chief executives rarely admit to watching the daily swings in their company’s share price. Archil Gachechiladze, however, has good reason to pay attention. If Lion Finance (BGEO) shares reach £105 in the coming days, its addition to the FTSE 100 at March’s reshuffle appears certain.

Even if the stock heads sideways from here – which, after doubling in a year and quadrupling in less than three, seems unlikely – entry looks like a matter of when rather than if. With a market capitalisation of £4.3bn, the banking group is worth roughly as much as the 90th stock in the index, Burberry (BRBY), which is ordinarily the threshold for automatic inclusion. Soon enough, exits of Beazley (BEZ) and Schroders (SDR) will free up space

“It happens in March or June or September, it doesn’t really matter,” Gachechiladze told Investors’ Chronicle this week. However, for the many followers of the UK’s blue-chip index – from active fund managers to retail investors grappling with what may be an unfamiliar name – the timing does matter. As passive trackers increase their demand for the shares, the choice to ignore the bank’s incredible market momentum becomes ever more consequential.

This also helps explain why more than 200 investors, including several City institutions, expressed interest in attending Lion Finance’s upcoming capital markets event in June within a day of the invite being sent on Monday. Though an excursion to Georgia’s Kakheti wine region may have added appeal, the professional probably recognise the need to evaluate the investment case. As should retail investors.

The Caucasian century

It’s a remarkable rise for a firm that was worth £500mn as recently as 2022. The same is true of its boss. If Lion Finance joine the index today, Gachechiladze would be its youngest chief executive. Despite his age, only Bill Winters of Standard Chartered (STAN) has run a UK-listed blue-chip lender for longer. Gachechiladze’s £61mn personal stake in the bank is also larger, in both absolute and relative terms, than that of any other bank chief.

After winning a bronze medal at the prestigious International Mathematical Olympiad aged 17, a career in academia beckoned. But when both Gachechiladze’s scientist parents lost their jobs, he swapped lanes for the security of business. Following roles in development finance, he won a scholarship to study for an MBA in the US, worked in UK private equity, and briefly served as deputy chief executive of TBC (TBCG), Lion Finance’s closest Georgian rival. He joined Bank of Georgia in 2009 as deputy chief executive of its corporate banking division, before eventually leading Georgia’s utilities and renewable power companies – both under the umbrella of what was then BGEO Group.

In 2018, BGEO split in two. The banking operation was renamed as Bank of Georgia, while the UK-listed investment arm, Georgia Capital (CGEO), retained its stake in the utilities utilities and power subsidiaries and a 20 per cent stake in the bank. Eight years on, Georgia Capital remains Lion Finance’s largest shareholder, with 16.9 per cent, though under the terms of the demerger, it has no board seat and has committed to vote in line with the bank, meaning it exerts no real control.

When he took over as chief executive in 2019 shortly after the split in 2019, Gachechiladze identified a need to invest in customer service and technology and improve a fragile leading market position and withering net promoter score. However, the reception from some non-Georgian was borderline hostile.

“I was kicked out of the room by a number of investors who said the only thing the company had going for it was a good cost-to-income ratio, and losing that wasn’t the way to start my new leadership,” he recalls.

Clearly, those investors had applied the then-dominant rationale for investing in the sector’s non-Georgian names, which was that cost-cutting offered the only real path to profitability at a time of fierce competition and ultra-low interest rates.

This attitude also revealed a weak appreciation for the strength of Georgia’s economy, which had grown 60 per cent in the decade to 2019 –equivalent to an average growth rate of 5 per cent a year at current prices. Thanks to booming tourism, trade and remittances, the economy more than doubled between 2020 and 2025, which to the IMF has lifted per-capita incomes from $4,310 to $10,130.

The significant extension of credit to both business and consumers has clearly also played a large role. Structurally, Lion Finance has benefited in two important ways. Among retail customers, its strong brand profile and proposition creates pricing power, while the lack of a mature debt capital market in the region means it can command a premium in corporate lending.

These factors – plus the Georgian central bank’s tolerance of a higher neutral rate of interest than much of the developed world – help explain why Lion Finance’s net interest margin sits at 6.2 per cent, roughly double the FTSE 100 average. At the same time, the group has kept a sound balance between investment and cost control: today, the cost-to-income ratio is below 36 per cent, or less than what it was in 2018.

The valuation

There are lots of reasons why Lion Finance shares appear so often in our stock screens. Not only does the business have momentum, but it is growing, and – against several metrics – very cheap.

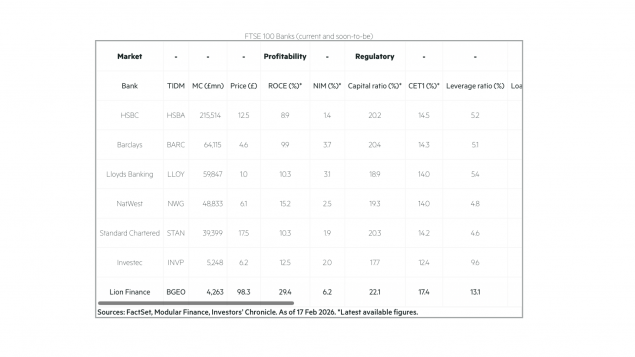

The group is also stunningly profitable. In the first nine months of 2025, it recorded a 27.9 per cent return on average tangible equity, making it more than twice as profitable as Barclays (BARC). Despite its higher margins, returns and capital buffers than the other FTSE 100 banks – as well as its much lower leverage (see table) – the stock continues to trade at less than seven times’ forecast earnings.

While a little above the five-year average, that’s below the all-time mean. Either way you slice it, it’s inexpensive for a stock whose earnings are growing at 15 per cent a year.

Georgia’s complicated geopolitics likely explains a lot. For more than a decade, domestic politics have been dominated by its richest man, Bidzina Ivanishvili, who was sanctioned by the US in 2024 for “undermining the democratic and Euro-Atlantic future of Georgia” for the benefit of Russia. Despite a ceasefire following its invasion in 2008, Russia continues to occupy a fifth of Georgia and according to the US State Department “influences Georgia’s economy via remittances, exports, and tourism”.

Lion Finance’s 2024 acquisition of Ameriabank, Armenia’s second largest lender – which explains the name change – probably didn’t change the risk profile for those fretful about the Caucasus, though a US-brokered peace agreement with Azerbaijan last August has at least put a lid on a long-running conflict.

Gachechiladze acknowledges the “problematic” nature of the neighbour to the north, though he is doubtful that an end to the war in Ukraine might precipitate a large flow of people and capital back out of Georgia. Instead, he points to the substantial international buy-in for development and investment in the region as a reason for optimism.

Reluctant to worry about the things outside his control, Gachechiladze says his biggest fear is “complacency, and the risk of not challenging each other internally”. The experience of the pandemic – when the Georgian lari fell 30 per cent against the dollar in a matter of days, and hard currency circulation briefly ground to a halt – clearly left a big impression, largely because it showed that adaptation under adverse conditions is possible.

For prospective investors, these questions might feel more binary. It’s also doubtful that credit expansion can continue at its recent pace forever, though as Georgia’s economy matures and its middle class grows, Gachechiladze says other financial services like wealth management will come into play.

Over in the UK, money managers such as JPMorgan, Schroders and M&G are now on the register. On balance, it seems likely more will soon follow.

Source: investorschronicle.co.uk

Other News

Lion Finance is heading to the big league, and this once-peripheral story is one worth knowing

20.02.2026.12:44

Chief executives rarely admit to watching the daily swings in their company’s share price. Archil Gachechiladze, however, has good reason to pay attention. If Lion Finance (BGEO) shares reach £105 in the coming days, its addition to the FTSE 100 at March’s reshuffle appears certain.

Even if the stock heads sideways from here – which, after doubling in a year and quadrupling in less than three, seems unlikely – entry looks like a matter of when rather than if. With a market capitalisation of £4.3bn, the banking group is worth roughly as much as the 90th stock in the index, Burberry (BRBY), which is ordinarily the threshold for automatic inclusion. Soon enough, exits of Beazley (BEZ) and Schroders (SDR) will free up space

“It happens in March or June or September, it doesn’t really matter,” Gachechiladze told Investors’ Chronicle this week. However, for the many followers of the UK’s blue-chip index – from active fund managers to retail investors grappling with what may be an unfamiliar name – the timing does matter. As passive trackers increase their demand for the shares, the choice to ignore the bank’s incredible market momentum becomes ever more consequential.

This also helps explain why more than 200 investors, including several City institutions, expressed interest in attending Lion Finance’s upcoming capital markets event in June within a day of the invite being sent on Monday. Though an excursion to Georgia’s Kakheti wine region may have added appeal, the professional probably recognise the need to evaluate the investment case. As should retail investors.

The Caucasian century

It’s a remarkable rise for a firm that was worth £500mn as recently as 2022. The same is true of its boss. If Lion Finance joine the index today, Gachechiladze would be its youngest chief executive. Despite his age, only Bill Winters of Standard Chartered (STAN) has run a UK-listed blue-chip lender for longer. Gachechiladze’s £61mn personal stake in the bank is also larger, in both absolute and relative terms, than that of any other bank chief.

After winning a bronze medal at the prestigious International Mathematical Olympiad aged 17, a career in academia beckoned. But when both Gachechiladze’s scientist parents lost their jobs, he swapped lanes for the security of business. Following roles in development finance, he won a scholarship to study for an MBA in the US, worked in UK private equity, and briefly served as deputy chief executive of TBC (TBCG), Lion Finance’s closest Georgian rival. He joined Bank of Georgia in 2009 as deputy chief executive of its corporate banking division, before eventually leading Georgia’s utilities and renewable power companies – both under the umbrella of what was then BGEO Group.

In 2018, BGEO split in two. The banking operation was renamed as Bank of Georgia, while the UK-listed investment arm, Georgia Capital (CGEO), retained its stake in the utilities utilities and power subsidiaries and a 20 per cent stake in the bank. Eight years on, Georgia Capital remains Lion Finance’s largest shareholder, with 16.9 per cent, though under the terms of the demerger, it has no board seat and has committed to vote in line with the bank, meaning it exerts no real control.

When he took over as chief executive in 2019 shortly after the split in 2019, Gachechiladze identified a need to invest in customer service and technology and improve a fragile leading market position and withering net promoter score. However, the reception from some non-Georgian was borderline hostile.

“I was kicked out of the room by a number of investors who said the only thing the company had going for it was a good cost-to-income ratio, and losing that wasn’t the way to start my new leadership,” he recalls.

Clearly, those investors had applied the then-dominant rationale for investing in the sector’s non-Georgian names, which was that cost-cutting offered the only real path to profitability at a time of fierce competition and ultra-low interest rates.

This attitude also revealed a weak appreciation for the strength of Georgia’s economy, which had grown 60 per cent in the decade to 2019 –equivalent to an average growth rate of 5 per cent a year at current prices. Thanks to booming tourism, trade and remittances, the economy more than doubled between 2020 and 2025, which to the IMF has lifted per-capita incomes from $4,310 to $10,130.

The significant extension of credit to both business and consumers has clearly also played a large role. Structurally, Lion Finance has benefited in two important ways. Among retail customers, its strong brand profile and proposition creates pricing power, while the lack of a mature debt capital market in the region means it can command a premium in corporate lending.

These factors – plus the Georgian central bank’s tolerance of a higher neutral rate of interest than much of the developed world – help explain why Lion Finance’s net interest margin sits at 6.2 per cent, roughly double the FTSE 100 average. At the same time, the group has kept a sound balance between investment and cost control: today, the cost-to-income ratio is below 36 per cent, or less than what it was in 2018.

The valuation

There are lots of reasons why Lion Finance shares appear so often in our stock screens. Not only does the business have momentum, but it is growing, and – against several metrics – very cheap.

The group is also stunningly profitable. In the first nine months of 2025, it recorded a 27.9 per cent return on average tangible equity, making it more than twice as profitable as Barclays (BARC). Despite its higher margins, returns and capital buffers than the other FTSE 100 banks – as well as its much lower leverage (see table) – the stock continues to trade at less than seven times’ forecast earnings.

While a little above the five-year average, that’s below the all-time mean. Either way you slice it, it’s inexpensive for a stock whose earnings are growing at 15 per cent a year.

Georgia’s complicated geopolitics likely explains a lot. For more than a decade, domestic politics have been dominated by its richest man, Bidzina Ivanishvili, who was sanctioned by the US in 2024 for “undermining the democratic and Euro-Atlantic future of Georgia” for the benefit of Russia. Despite a ceasefire following its invasion in 2008, Russia continues to occupy a fifth of Georgia and according to the US State Department “influences Georgia’s economy via remittances, exports, and tourism”.

Lion Finance’s 2024 acquisition of Ameriabank, Armenia’s second largest lender – which explains the name change – probably didn’t change the risk profile for those fretful about the Caucasus, though a US-brokered peace agreement with Azerbaijan last August has at least put a lid on a long-running conflict.

Gachechiladze acknowledges the “problematic” nature of the neighbour to the north, though he is doubtful that an end to the war in Ukraine might precipitate a large flow of people and capital back out of Georgia. Instead, he points to the substantial international buy-in for development and investment in the region as a reason for optimism.

Reluctant to worry about the things outside his control, Gachechiladze says his biggest fear is “complacency, and the risk of not challenging each other internally”. The experience of the pandemic – when the Georgian lari fell 30 per cent against the dollar in a matter of days, and hard currency circulation briefly ground to a halt – clearly left a big impression, largely because it showed that adaptation under adverse conditions is possible.

For prospective investors, these questions might feel more binary. It’s also doubtful that credit expansion can continue at its recent pace forever, though as Georgia’s economy matures and its middle class grows, Gachechiladze says other financial services like wealth management will come into play.

Over in the UK, money managers such as JPMorgan, Schroders and M&G are now on the register. On balance, it seems likely more will soon follow.

Source: investorschronicle.co.uk